Triglav Group maintains stable and successful operations in this year's challenging environment.

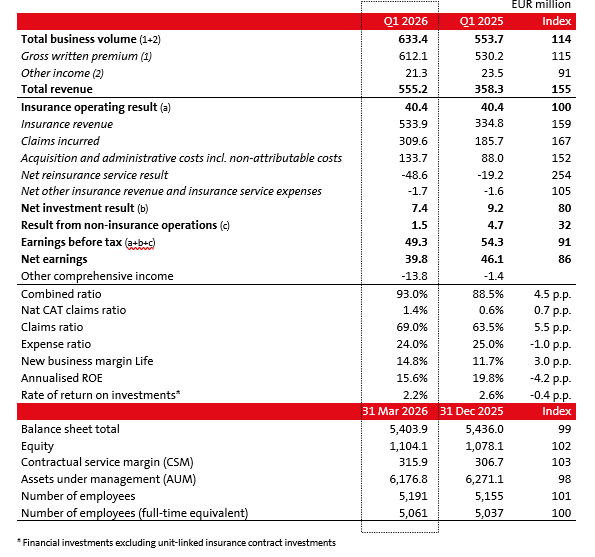

- Triglav Group's total business volume increased by 14%

year-on-year to EUR 633.4 million, primarily

driven by strong premium growth in

international markets.

- Earnings before tax amounted to EUR 49.3 million (Q1 2025: EUR 54.3 million), while net

earnings amounted to EUR 39.8 million (Q1 2025: EUR 46.1 million). Taking into

account the anticipated business conditions for the remainder of the year, Triglav

Group estimates that it will achieve its planned annual earnings before tax for

2026 (EUR 170–190 million).

- The combined ratio stood at 93.0% (Q1 2025: 88.5%),

while the new business margin Life was 14.8% (Q1 2025: 11.7%). Annualised

return on equity stood at 15.6% (Q1 2025: 19.8%).

- Capital adequacy remained within the target range of

200–250% at the end of the first quarter.

- The proposed dividend for 2026 amounts to EUR 3.00 gross per share, totalling EUR 68.2 million (7% higher than in the previous year), which, in line with the dividend policy, represents half of consolidated net earnings for 2025. The expected dividend payment date is 17 June 2026. The General Meeting of Shareholders is scheduled to take place on 2 June 2026.

Andrej Slapar, President of the Management Board of Zavarovalnica Triglav, commented:

"We are satisfied with the results achieved; earnings before tax amounted to EUR 49.3 million and, taking into account the anticipated conditions for the remainder of the year, we expect to achieve our annual profit guidance.

Our operations in the first quarter of this year took place in more challenging conditions than last year, primarily due to volatility in financial markets and somewhat higher CAT claims. Stable and profitable operations were maintained in the insurance business. In the investment business, we were exposed to financial market volatility and therefore managed risks and the investment portfolio with particular care. Capital strength and financial stability were effectively maintained.

In line with our strategy, we continue to strengthen our business volume and share outside Slovenia. In international insurance markets, we cooperate with numerous partners and adapt dynamically to opportunities and market conditions, resulting in potentially volatile business volumes from year to year.

This year, we will propose a dividend payment to the General Meeting of Shareholders in line with our attractive and sustainable dividend policy. Through it, we also pursue our commitment to creating value for shareholders.

We remain focused on achieving our strategic ambitions. I would like to take this opportunity to thank our employees, whose dedication and expertise make a significant contribution to their realisation."FINANCIAL HIGHLIGHTS FOR Q1 2026

Triglav Group increased its total business volume by 14% to EUR 633.4 million. Gross written premium increased by 15% to EUR 612.1 million.

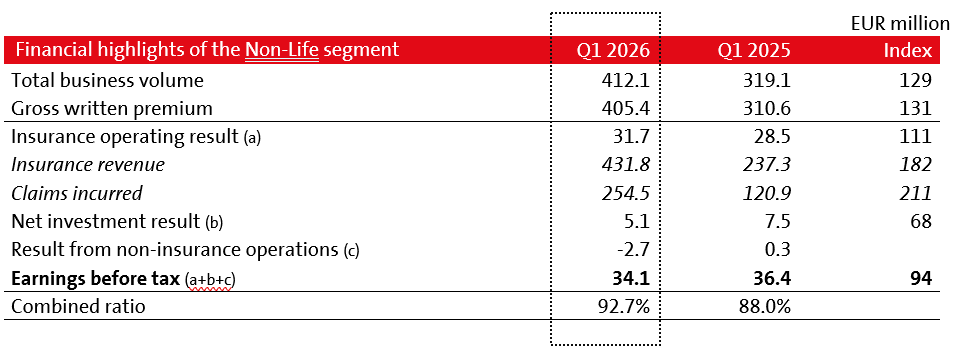

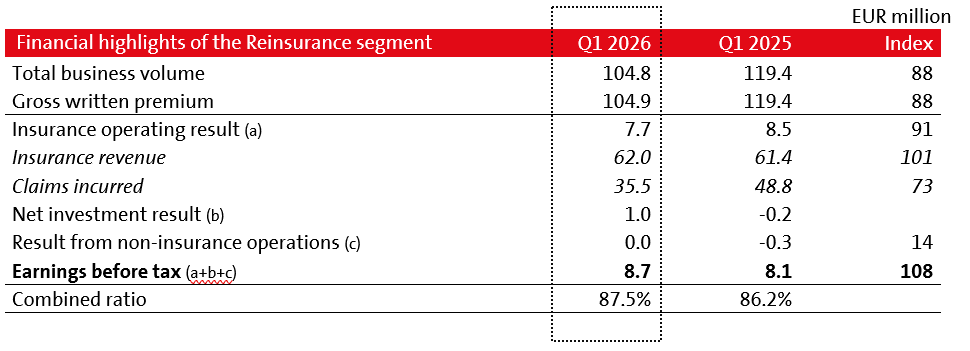

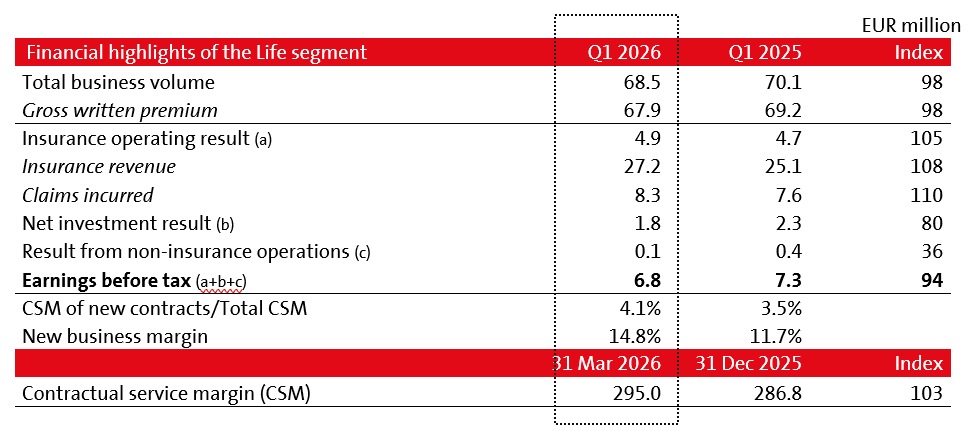

By business segment [*], the Non-Life segment recorded the highest growth in business volume, at 29% (EUR 412.1 million), primarily driven by high premium growth in international markets. The Reinsurance segment's business volume amounted to EUR 104.8 million, down 12% compared to the same period last year, mainly due to year-on-year fluctuations in the renewals of certain reinsurance contracts. The Life segment generated EUR 68.5 million in business volume, 2% lower than in the previous year; despite strong growth in traditional life insurance across all markets, the total business volume was primarily affected by a decline in unit-linked life insurance premium. The Health segment increased its business volume by 14% to EUR 17.6 million, while the Asset Management segment recorded growth of 2% to EUR 30.3 million.

In line with strategic ambitions, Triglav strengthened its business volume outside Slovenia. The share of the Slovenian market declined to 48% (Q1 2025: 55%), the share of the Adria region markets excluding Slovenia was 17% (Q1 2025: 18%), while the share of international markets increased to 35% (Q1 2025: 28%). Of this, 19% of business was generated in international insurance markets and 17% in international reinsurance markets.

Triglav increased its business volume in all markets in the Adria region except Montenegro, mainly due to year-on-year fluctuations in the renewal of certain contracts. On the Slovenian market, growth amounted to 1%, while on other Adria markets it reached 8%. In international insurance markets, business volume increased by 257% to EUR 117.4 million, of which 78% was generated in the Italian market. In international reinsurance markets, business volume decreased by 12% to EUR 104.9 million.

Triglav Group's earnings before tax amounted to EUR 49.3 million (Q1 2025: EUR 54.3 million), while net earnings amounted to EUR 39.8 million (Q1 2025: EUR 46.1 million). The business result was influenced by higher business volume, a somewhat lower investment result and increased claims development, including a higher level of CAT claims. Three CAT events were estimated at EUR 7.1 million (Q1 2025: EUR 2.0 million), of which storms in Slovenia caused EUR 5.1 million in claims, while reinsurance nat CAT claims amounted to an estimated EUR 2.0 million.

Triglav operated profitably in all segments except the Health segment. The majority of earnings before tax was generated by the insurance business. At EUR 40.4 million, they were comparable to the previous year, while the Non-Life and Life segments improved their results. Earnings before tax from the investment business totalled EUR 7.4 million (Q1 2025: EUR 9.2 million), while earnings before tax from non-insurance operations amounted to EUR 1.5 million (Q1 2025: EUR 4.7 million, also influenced by one-off events). Zavarovalnica Triglav, Triglav Group's parent company, generated earnings before tax of EUR 30.7 million (Q1 2025: EUR 39.5 million) and net earnings of EUR 25.0 million (Q1 2025: EUR 33.0 million).

*At the beginning of the reporting period, Triglav Group adjusted the presentation of its business segments – the previously single Non-Life segment was split into the Non-Life segment and a new Reinsurance segment. The latter is gaining in strategic importance and scale in international operations and is characterised by distinct business features. Comparative data have been restated accordingly to reflect adjustments to internal reporting.

Other comprehensive income amounted to EUR –13.8 million (Q1 2025: EUR –1.4 million), with its lower level driven by geopolitical shocks, reflected in changes in interest rates and their impact primarily on the revaluation of investments at the end of the quarter. Triglav Group's capitalisation was within the target range of 200–250% at the end of the first quarter.

The combined ratio stood at a favourable 93.0% (Q1 2025: 88.5%), or 88.2% on a comparable basis excluding the new business with partner Prima Assicurazioni in the Italian market launched in June last year. The nat CAT claims ratio more than doubled, increasing from 0.6% to 1.4%. The claims ratio increased by 5.5 percentage points, rising across all three segments, i.e. Non-Life, Reinsurance and Health, with the most pronounced increase in the latter. The expense ratio decreased by 1.0 percentage point to 24.0%, as the growth in insurance revenue outpaced the growth in expenses. Triglav maintained or improved favourable profitability of the insurance business across all markets in the Adria region.

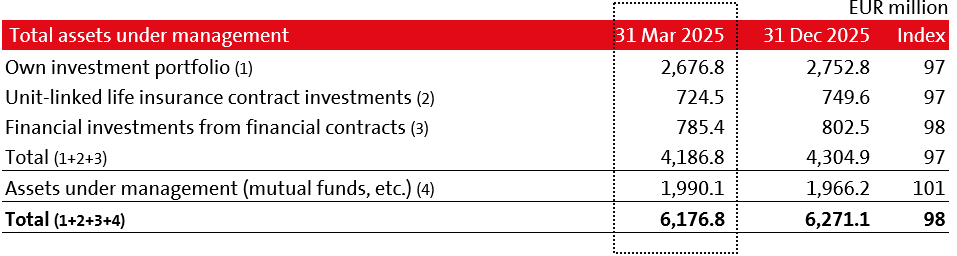

Total assets under management remained broadly unchanged in composition compared to the end of the previous year. They stood at EUR 6.2 billion, down 2% compared to 31 December 2025. The investment portfolio was adversely affected by the increase in required bond yields and the decline in international equity indices. The rate of return on investments (excluding unit-linked insurance assets) was 2.2%, down by 0.4 percentage points year-on-year. It was positively impacted by higher interest income, while volatile financial market conditions adversely affected the rates of return on the equity portfolio.

TRIGLAV GROUP PERFORMANCE BY SEGMENT

Uroš Ivanc, a Management Board member of Zavarovalnica Triglav, said:

"Operations across all segments continue to be developed in line with the strategy. The Non-Life segment remains the main driver of growth, further supported by expansion into international insurance markets. In the first quarter, we increased the volume of this segment and maintained its robust profitability. The segment's somewhat lower result reflected increased claims development resulting from international business and a higher level of CAT claims, while volatile financial market conditions affected the investment result and portfolio value.

We are strategically strengthening reinsurance and therefore now report it as a separate segment. Its business volume declined somewhat compared to the same period last year due to the dynamics of business with some partners, while favourable profitability was maintained and earnings increased.

The Life and Asset Management segments remain stable, although their results in the first quarter were affected by unfavourable conditions in the financial markets. In the Life segment, growth was recorded in markets outside Slovenia and the new business margin increased, while in the Asset Management segment income from fees continued to grow steadily.The Health segment remains in an intensive development phase, with a gradual build-up of a sufficiently large portfolio. As expected, it reported a negative operating result for the period."

Non-Life segment

- Total business volume increased by 29% to EUR 412.1 million.

- Combined ratio stood at favourable 92.7% (Q1 2025: 88.0%).

- Earnings before tax reached EUR 34.1 million, down by 6% year-on-year.

The total business volume increased by 29% to EUR 412.1 million, while written premium rose by 31%, with growth achieved across most Non-Life insurance lines. By market, international markets recorded growth of as much as 257%, with the largest volume generated in the Italian market (EUR 91.5 million). In Slovenia, premium increased by 3%, while in other Adria markets it rose by 6%.

Claims incurred increased by 111% to EUR 254.5 million, primarily due to higher reported claims from the larger international insurance portfolio and CAT events (the nat CAT claims ratio increased from zero in the previous year to 1.2%).

The combined ratio Non-Life stood at a favourable 92.7%. Compared to the first quarter of the previous year, it increased by 4.7 percentage points, primarily due to a higher claims ratio as a result of increased claims incurred and a weaker reinsurance result. The expense ratio declined, mainly due to stronger growth in insurance revenue relative to expenses and improved net claims development. Excluding business in the Italian market through Prima, the combined ratio would have stood at 86.1%, which is 1.9 percentage points better than in the previous year.

Earnings before tax declined by 6%, reaching EUR 34.1 million. The insurance operating result increased significantly, primarily due to higher business volume and changes in the portfolio structure. At the same time, the net investment result declined, mainly due to unrealised losses on financial assets (declines in the market value of existing investments), despite higher interest income.

Reinsurance segment

- Total business volume amounted to EUR 104.8 million, down 12% year-on-year.

- Combined ratio stood at favourable 87.5% (Q1 2025: 86.2%).

- Earnings before tax rose by 8%, reaching EUR 8.7 million.

The total business volume decreased by 12% to EUR 104.8 million; written premium showed a similar trend, mainly due to year-on-year fluctuations in business with some larger partners.

The combined ratio Reinsurance stood at a favourable 87.5%, up 1.4 percentage points compared to the previous year. This was primarily due to a higher claims ratio as a result of a weaker reinsurance result, while the expense ratio declined due to faster growth in insurance revenue than in expenses. The nat CAT claims ratio decreased by 0.1 percentage points to 3.2%.

Earnings before tax rose by 8%, reaching EUR 8.7 million. The insurance operating result was slightly lower than in the previous year, while the net investment result was more favourable due to positive exchange rate differences on financial investments.

Life segment

- Total business volume amounted to EUR 68.5 million, representing a 2% decrease year-on-year.

- New business margin stood at a favourable 14.8% (Q1 2025: 11.7%). Contractual service margin increased by 3%, reaching EUR 295.0 million.

- Earnings before tax amounted to EUR 6.8 million, down 6% year-on-year.

The total business volume of EUR 68.5 million decreased by 2%, as did the life insurance premium. While traditional life insurance recorded strong growth, the total business volume was primarily affected by a decline in unit-linked life insurance premium, resulting from different dynamics of sales campaigns through the bank sales channel.

The new business margin increased by 3.0 percentage points to a favourable 14.8%, primarily due to a higher volume of premium from newly written term life insurance contracts, which have higher profitability than unit-linked life insurance contracts.

The contractual service margin, amounting to EUR 295.0 million (i.e. the expected future profit from insurance contracts already concluded), increased by 3%, primarily due to an improved estimate of future cash flows from the existing insurance portfolio.

The CSM of new contracts (i.e. the expected future profit from newly concluded insurance contracts) represented 4.1% of the total contractual service margin, up 0.5 percentage points year-on-year. It amounted to EUR 12.0 million, of which 39% related to unit-linked life insurance. The release of the contractual service margin (i.e. the gradual recognition of this profit over time) to profit or loss amounted to EUR 10.6 million, compared to EUR 9.3 million in the same period last year.

Earnings before tax of the Life segment declined by 6%, reaching EUR 6.8 million. The insurance operating result increased by 5%, primarily due to growth in markets outside Slovenia. The net investment result decreased by 20%, primarily due to the decline in the value of equity investments resulting from financial market conditions.

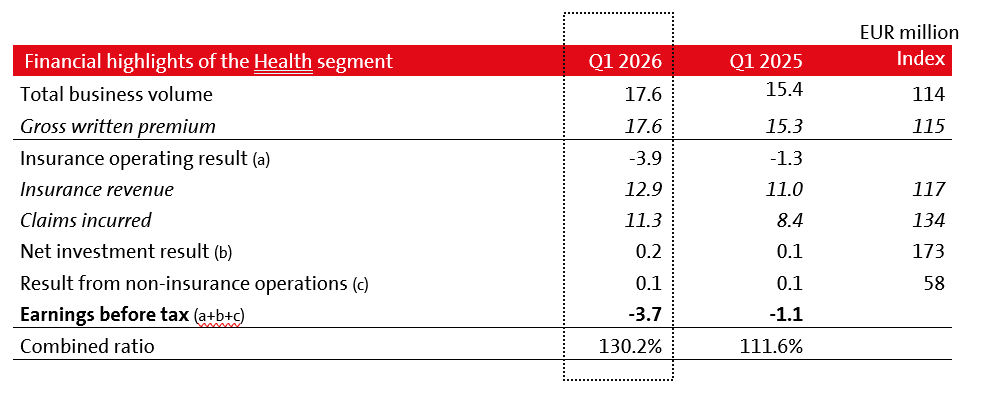

Health segment

- Total business volume increased by 14% to EUR 17.6 million.

- Combined ratio stood at 130.2% (Q1 2025: 111.6%).

- Earnings before tax amounted to EUR –3.7 million (Q1 2025: EUR –1.1 million).

Following the restructuring of the segment's business model in 2024, Triglav continues activities aimed at the growth and development of complementary health insurance products in Slovenia and other markets in the region. Triglav expects the Health segment's result to remain volatile going forward, as the segment is in a phase of strong growth and still relatively limited business volume.

The total business volume increased by 14% to EUR 17.6 million, with written premium recording similar growth. Growth was achieved in most markets.

The combined ratio Health stood at 130.2% compared to 111.6% in the same period last year, with the increase mainly attributable to a higher claims ratio.

Earnings before tax amounted to EUR –3.7 million (Q1 2025: EUR –1.1 million). The segment's negative result primarily originated from the insurance business, mainly due to higher claims incurred resulting from portfolio growth, the number of loss events and higher prices charged by healthcare service providers. The segment's result was positive in the investment business and in non-insurance operations.

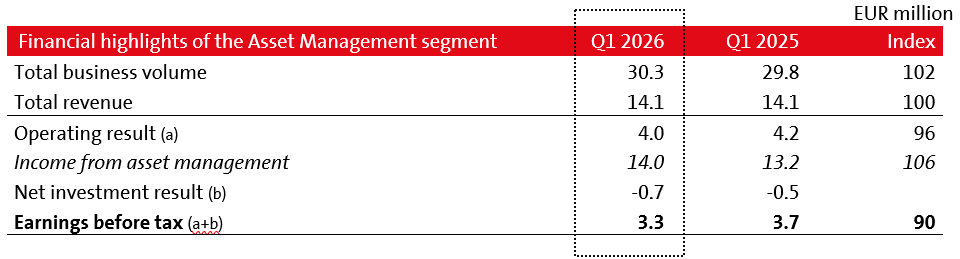

Asset Management segment

- Total business volume increased by 2% to EUR 30.3 million.

- Income from asset management rose by 6% to EUR 14.0 million.

- Earnings before tax declined by 10%, reaching EUR 3.3 million.

The total business volume increased by 2% to EUR 30.3 million, driven by a higher volume of voluntary pension insurance concluded and higher income from asset management, i.e. fees.

Earnings before tax declined by 10%, reaching EUR 3.3 million. The result was affected by 6% higher fees and a negative net investment result due to higher provisions for cases where the guaranteed return on certain insurance products is not achieved.

Triglav Group's total assets under management as at 31 March 2026 amounted to EUR 6.2 billion, representing a 2% decrease relative to 31 December 2025.

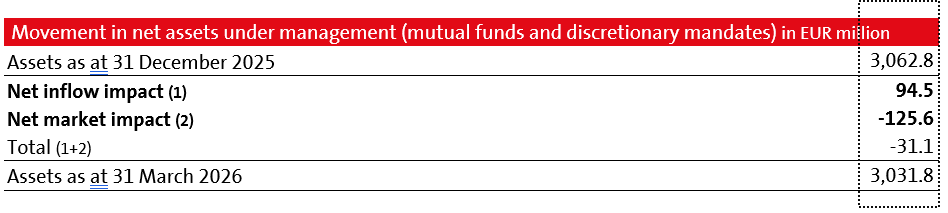

The volume of assets under management in mutual funds and discretionary mandate assets was favourably affected by client net inflows and negatively affected by financial market conditions.

PLAN FOR 2026 AND STRATEGY TO 2030 (financial highlights)

Earnings before tax:

- 2026 plan: EUR 170–190 million (guidance reaffirmed following Q1 results)

- Strategy to 2030: EUR 250–300 million

Total business volume:

- 2026 plan: more than EUR 2.4 billion

- Strategy to 2030: EUR 2.5–3.0 billion in 2030

Assets under management:

- Strategy to 2030: more than EUR 10 billion

Combined ratio:

- 2026: around 95%

- Strategy to 2030: below 95% over the strategy period

Return on equity:

- Strategy to 2030: 12–13% in 2030